All About: What Is Contribution Margin?

Nov 11, 2023 By Susan Kelly

Introduction

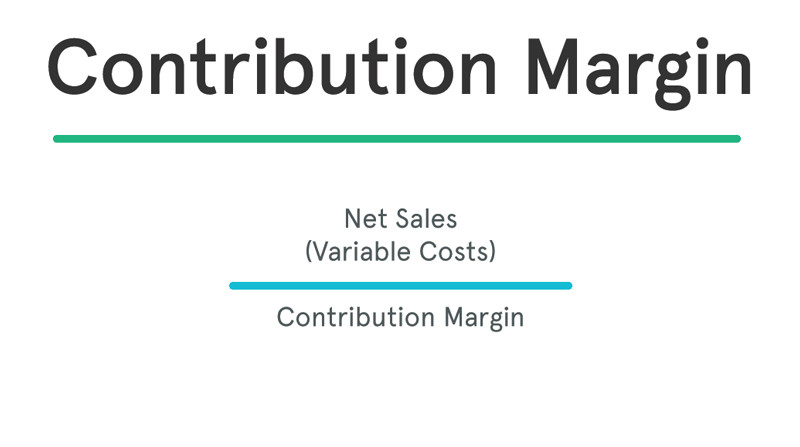

What Is Contribution Margin? The incremental profit from each unit sold is known as the "contribution margin," calculated by subtracting the product's price from any associated variable costs. A company's contribution margin is the amount of money it has left over after covering all its fixed costs and investing in growth. Increasing a company's contribution margin is a tried and true method of profit planning that can help a business turn a profit even if sales are down.

Example of Contribution Margin

Assume that a machine used to produce ink pens costs $10,000. It costs $0.2 in raw materials like plastic, ink, and nib to make one ink pen, $0.1 in power to run the machine that makes it, and $0.3 in labour to make that one ink pen. Every unit's variable cost is made up of these three factors. Ink pens have a total variable production cost of $0.6 per unit, or ($0.2 + $0.1 + $0.3). Producing one hundred ink pens incurs a total variable cost of $60 ($0.6 * 100 units) while producing ten thousand incurs a total cost of $6,000 ($0.6 * 10,000 units). In general, variable costs rise as production scales up.

Contribution

C is the Unit Contribution Margin, which is calculated as Unit Revenue (Price) minus the Variable Cost per Unit (V). Unit contribution over unit pricing or total contribution over total revenue yield the Contribution Margin Ratio. With a price of $10 and a variable cost of $2 per unit, the contribution margin per unit is $8, and the contribution margin ratio is $8/$10, or 80%. Revenue is defined as income-less expenses that are constant throughout time. The term "contribution margin" refers to the percentage of revenue covering fixed expenses. Alternately, the unit contribution margin is the slope of the profit line and represents the amount each unit sale contributes to the overall profit.

Contribution margin = (Net product revenue - Product variable costs) Product revenue

How Contribution Margin Works

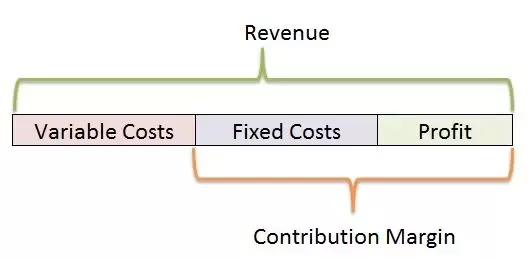

To measure the impact of pricing, sales volume, and overhead on a company's bottom line, analysts use a metric called contribution margin, a component of the broader cost-volume-profit (CVP) framework. Operating profit can be calculated using the following formula:

Income from Operations = Total Revenue. Total Variable Expenses minus Total Expenses that are Fixed

When viewed in this manner, operating profit allows a company to analyse the effects of changes in sales, variable costs, and fixed costs on the bottom line. There are two main types of expenses: those that are fixed and those that are subject to change. The contribution margin is calculated by deducting the cost of goods sold (which includes variable costs) from the total revenue.

How Important is Contribution Margin in Business?

Contribution margin is commonly utilised in cost-benefit analyses when businesses determine a product's selling price. The contribution margin must be significant to pay the business's fixed costs. If the contribution margin for a product line or business is low or negative, production of that line or company should be discontinued unless sales volumes are extremely high. Analysis of breakeven or desired income requires consideration of the contribution margin. By dividing fixed costs by the contribution margin per unit, a target number of units must be sold for the business to break even. Given a company's limited resources, determining which of its goods yields the highest contribution margin can help break a stalemate. Products with a more significant contribution margin are prioritised.

What Mistakes Do People Make?

There are "so many possibilities to make a mistake" because "costs don't fall cleanly into fixed and variable categories," and certain costs are instead "quasi-variable." To improve output momentarily, you can, for instance, introduce a new piece of machinery into the assembly line. It's not quite either a fixed cost because it's a one-time purchase that doesn't change with the amount of product you're creating, nor is it an additional cost because of the increased production (and thus variable). This may be said of some incomes on occasion as well. A financial analyst's decision about how to categorise these wages demands some degree of expert discretion. Research and development budgets are also under review. Others see them as direct product costs, while others classify them as fixed costs. Changes in how these expenses are accounted for could have a significant impact on your contribution margin.

Conclusions

A product's contribution margin is the amount of its sales income covering fixed costs rather than variable ones. Break-even analysis relies heavily on the concept of contribution margin. Companies that rely heavily on human labour but have minimal fixed costs have low contribution margins, while those that rely heavily on capital equipment and manufacturing have larger contribution margins due to higher fixed costs.

Susan Kelly Dec 07, 2023

Online Solutions for Cashing Checks

34724

Triston Martin Oct 04, 2023

Most Reliable Exchange Traded Funds For Commodities

80773

Susan Kelly Dec 04, 2023

Navigating the Basics of Phillips Curve: A Detailed Guide

38757

Susan Kelly Feb 25, 2024

What Does Real Estate Agent Do

1207

Triston Martin Nov 22, 2023

Navigating Charge-Offs: Understanding, Impact, and How to Deal With Them.

47844

Susan Kelly Oct 15, 2023

Jewelry Insurance: All the Information You Need

25403

Triston Martin Dec 12, 2023

Stocks That Are Giving Investors Big Buybacks

89802

Triston Martin Feb 05, 2024

How Can You Pay Your Property Tax Bill?

46014